Oh Sh*t, My App is Successful and I Didn’t Think About Accessibility

Plus, more links to make you a little bit smarter today.

The enduring horror of monster encounters in Saturnalia

“How Santa Ragione used a less is more approach to monster encounters in its indie horror title Saturnalia.”

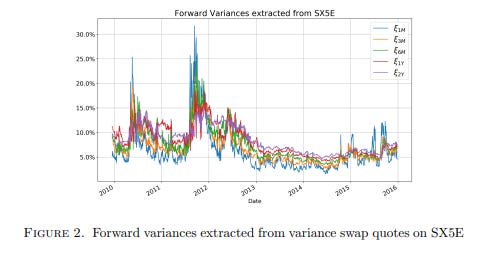

RISK PREMIUM AND ROUGH VOLATILITY

“One the one hand, rough volatility has been shown to provide a consistent framework to capture the properties of stock price dynamics both under the historical measure and for pricing purposes. On the other hand, market price of volatility risk is a well-studied object in Financial Economics, and empirical estimates show it to be stochastic rather than deterministic. Starting from a rough volatility model under the historical measure, we take up this challenge and provide an analysis of the impact of such a non-deterministic risk for pricing purposes.”

Oh Sh*t, My App is Successful and I Didn’t Think About Accessibility

“Speedrunning a11y in SwiftUI”

Sparse Index Tracking: Simultaneous Asset Selection and Capital Allocation via ℓ0-Constrained Portfolio

“Sparse index tracking is a prominent passive portfolio management strategy that constructs a sparse portfolio to track a financial index. A sparse portfolio is preferable to a full portfolio in terms of reducing transaction costs and avoiding illiquid assets. To achieve portfolio sparsity, conventional studies have utilized ℓp-norm regularizations as a continuous surrogate of the ℓ0-norm regularization. Although these formulations can construct sparse portfolios, their practical application is challenging due to the intricate and time-consuming process of tuning parameters to define the precise upper limit of assets in the portfolio.

In this paper, we propose a new problem formulation of sparse index tracking using an ℓ0-norm constraint that enables easy control of the upper bound on the number of assets in the portfolio. Moreover, our approach offers a choice between constraints on portfolio and turnover sparsity, further reducing transaction costs by limiting asset updates at each rebalancing interval. Furthermore, we develop an efficient algorithm for solving this problem based on a primal-dual splitting method. Finally, we illustrate the effectiveness of the proposed method through experiments on the S&P500 and Russell3000 index datasets.”

Entropy corrected geometric Brownian motion

“The geometric Brownian motion (GBM) is widely employed for modeling stochastic processes, yet its solutions are characterized by the log-normal distribution. This comprises predictive capabilities of GBM mainly in terms of forecasting applications. Here, entropy corrections to GBM are proposed to go beyond log-normality restrictions and better account for intricacies of real systems. It is shown that GBM solutions can be effectively refined by arguing that entropy is reduced when deterministic content of considered data increases. Notable improvements over conventional GBM are observed for several cases of non-log-normal distributions, ranging from a dice roll experiment to real world data”