Four ways to build better indie marketing campaigns

Four ways to build better indie marketing campaigns

Plus, more links to make you a little bit smarter today.

Four ways to build better indie marketing campaigns

“20ten's director of gaming Luke Fisher gives tips on how to keep players engaged”

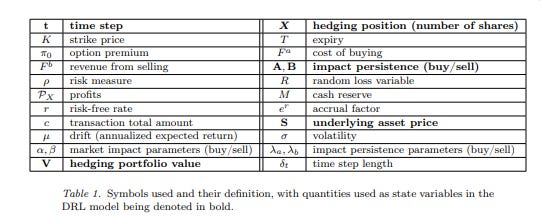

Deep Hedging with Market Impact

“Dynamic hedging is the practice of periodically transacting financial instruments to offset the risk caused by an investment or a liability. Dynamic hedging optimization can be framed as a sequential decision problem; thus, Reinforcement Learning (RL) models were recently proposed to tackle this task. However, existing RL works for hedging do not consider market impact caused by the finite liquidity of traded instruments. Integrating such feature can be crucial to achieve optimal performance when hedging options on stocks with limited liquidity.

In this paper, we propose a novel general market impact dynamic hedging model based on Deep Reinforcement Learning (DRL) that considers several realistic features such as convex market impacts, and impact persistence through time. The optimal policy obtained from the DRL model is analysed using several option hedging simulations and compared to commonly used procedures such as delta hedging. Results show our DRL model behaves better in contexts of low liquidity by, among others: 1) learning the extent to which portfolio rebalancing actions should be dampened or delayed to avoid high costs, 2) factoring in the impact of features not considered by conventional approaches, such as previous hedging errors through the portfolio value, and the underlying asset’s drift (i.e. the magnitude of its expected return).”

Sizing the bets in a focused portfolio

“The paper provides a mathematical model and a tool for the focused investing strategy as advocated by Buffett [1], Munger [2], and others from this investment community. The approach presented here assumes that the investor’s role is to think about probabilities of different outcomes for a set of businesses. Based on these assumptions, the tool calculates the optimal allocation of capital for each of the investment candidates. The model is based on a generalized Kelly Criterion with options to provide constraints that ensure: no shorting, limited use of leverage, providing a maximum limit to the risk of permanent loss of capital, and maximum individual allocation. The software is applied to an example portfolio from which certain observations about excessive diversification are obtained. In addition, the software is made available for public use.”

About Ideas Now

Neat idea — this website basically scrapes personal blogs that have some sort of “what I’m working on” page and places it here in one searchable database. I plan on going through a couple of these and seeing if anything strikes my interest — always on the lookout for new blogs. Who knows, maybe I’m already on here!

Finding Near-Optimal Portfolios With Quality-Diversity

“The majority of standard approaches to financial portfolio optimization (PO) are based on the mean-variance (MV) framework. Given a risk aversion coefficient, the MV procedure yields a single portfolio that represents the optimal trade-off between risk and return. However, the resulting optimal portfolio is known to be highly sensitive to the input parameters, i.e., the estimates of the return covariance matrix and the mean return vector. It has been shown that a more robust and flexible alternative lies in determining the entire region of near-optimal portfolios. In this paper, we present a novel approach for finding a diverse set of such portfolios based on quality-diversity (QD) optimization. More specifically, we employ the CVT-MAP-Elites algorithm, which is scalable to high-dimensional settings with potentially hundreds of behavioral descriptors and/or assets. The results highlight the promising features of QD as a novel tool in PO.”